AI Diffusion into the Feed

AI-powered Chinese Mini-Dramas and the Attention Economy

Over the Lunar New Year break, the parent company of TikTok, ByteDance, released its latest text-to-image and text-to-video model and app called Seedance 2.0. Its debut was so good it sent shockwaves across Hollywood and sparked deep anxiety over the fast-evolving capabilities of AI. And soon after its release, movie studios such as Paramount and Disney sent angry letters to ByteDance for copyright infringement concerns.

Although the primary commercial potential of these new Chinese models is not yet in major large screen production, as Hollywood most fears, it is being widely adopted by a new media channel that China dominates: microdramas.

The MIT Tech Review last year reported on the rise of micro-drama exports from China last year. Microdramas are smartphone-native, have a fast turnaround, and are directly competitive for viewers’ attention and time. They are not “shorter TV shows,” they are a new vertical of their own.

These micro-dramas exploded in part due to timing: the phone became the living room, distribution became adept at buying attention, and production pipelines learned to optimize for retention at scale.

And because people don’t choose what to watch with their thumbs at 11:30 pm — they often turn on whatever is frictionless and emotionally legible in a phone-sized frame.

According to DataEye, a Chinese media analytics firm, over 300 million downloads of Chinese micro-drama apps globally pushed YouTube and Netflix off the top of app store rankings in the first half of 2025. Some of the most notable micro-drama Chinese platform names include ReelShort, DramaBox, GoodShort, and ShortMax. Most of the parent companies behind these platforms produce content in Chinese and English as they distribute across different social media platforms aimed at different audience demographics. But ReelsShort, ShortMax, and so focuses on the English-native market.

Similar to American short-form native platform Quibi, the leading Chinese micro-drama company Reelshort also targets mobile-first, short-form, vertical-video entertainment, but the main difference in their strategies lies in their approach. While Quibi failed with high-budget, A-list content, ReelShort thrived on ultra-low-budget, addictive, soapy, “guilty pleasure” dramas.

For the sake of research, I watched a few episodes and realized its addictive nature. The themes read like a speedrun of narrative dopamine: car crash amnesia, comeback revenge arcs, double lives, fake marriages, cheating spouses. Honestly, the more dramatic and emotionally triggering, the more engaging. They’re like the less polished, more spiteful cousins of K-drama tropes, and they remind me of the telenovelas that used to play in the background at my friend’s house. Each episode was a wild ride; it gave you dopamine, cortisol, oxytocin, adrenaline, all in 120 seconds of your life. Each episode feels short, but follow along for a whole storyline, and you’ve burned through an hour without noticing. Reelshort’s slogan “every second is drama” is quite literal in that time is attention and attention is the business.

And just when you’re super amped up and hooked, it displays a black screen to unlock the next episode, pay a few coins, or watch an ad. Micro-dramas are not just shorter TV series. The content business now looks more like the economics of gaming. As you’re already hooked, you are presented with two options to continue your show: pay upfront, or watch an ad to unlock the next episode.

The Business of Microdramas

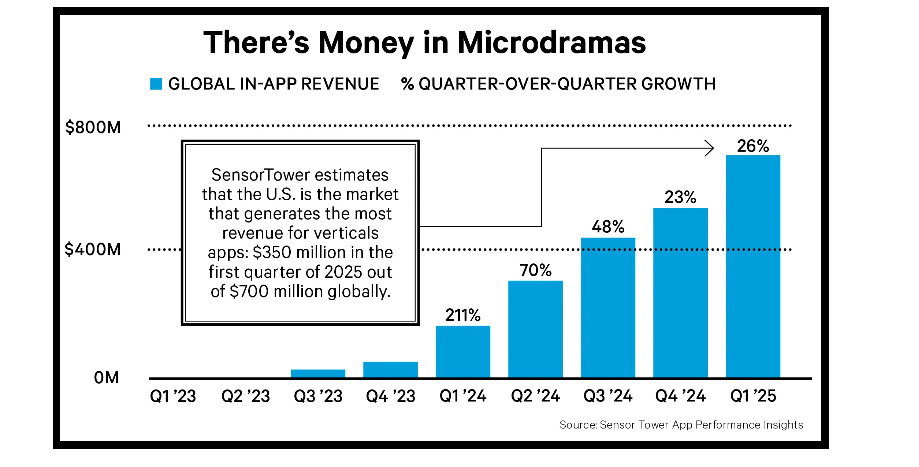

Microdramas are both an advertising business and a subscription business. And it isn’t a small business. DataEye estimates that China’s microdramas + “manju” (AI/animated short dramas) generated over RMB 100 billion in annual output value—well above the earlier market expectation of ~RMB 60 billion. At that scale, the microdrama industry is 2× China’s domestic film box office annual revenue of RMB 51.832 billion.

Chart: The Hollywood Reporter

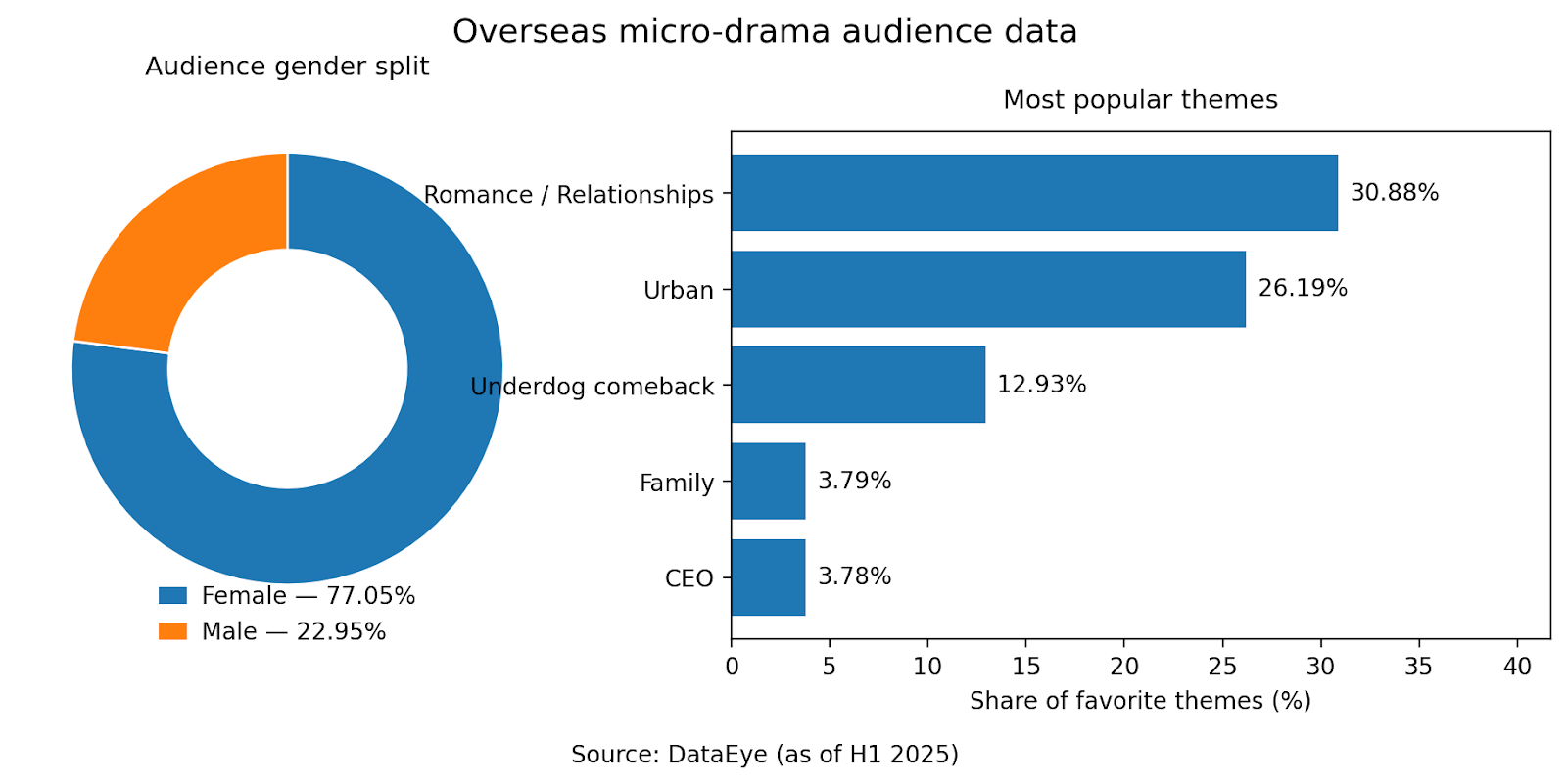

According to a Chinese business publication, The Paper’s report, Chinese micro-dramas have reached 200+ countries and regions. In 2025, Guangda Securities estimates that the overseas market generated ~US$2.38B in revenue on 1.21B downloads, with revenue growth accelerating to +263% year-on-year and download growth to +135% year-on-year. As of now, North America remains the main profit pool, contributing over 60% of overseas revenue for these companies, while Southeast Asia leads in share at ~35%, with the Middle East, Japan, Korea, and Europe also cited as expanding rapidly.

Amongst the top platforms by revenue are ReelShort, DramaBox, and GoodShort. The three platforms together account for over 53% of the market.

Embracing AI

Today, companies like ReelShort still mostly rely on Western actors when making content for Western audiences. But the next step, which many have told investors they plan to take, is to use AI to create characters to perform these manuscripts, thereby significantly reducing production and export costs and reshaping the economics of microdramas.

The most recent generation of Chinese video models certainly seems capable of making this leap. The internet has already been thrown into a frenzy as snippets of short period dramas leaked ahead of Seedance’s latest update announcements, as well as new action films created completely on Kling. Tutorials on how to turn written scripts into videos using these tools have also flooded X. Hugging Face’s head of the APAC ecosystem, Tiezhen Wang, is also sharing videos that resemble scenes from a Hollywood blockbuster created by Seedance 2.0. There was even a dedicated AI Film Festival hosted in India by InVideo as part of the broader India AI Impact Summit, which included PM Modi, President Macron, Jensen Huang, Sam Altman, and Sundar Pichai in attendance. Of course, AI sometimes still produces horrendous glitches. However, some argue that whether the protagonist was wearing the same t-shirt in two consecutive scenes doesn’t affect the experience of a one-minute short meant to be watched on a 1080p phone screen.

And this is no longer just hypothetical. In mid-March, ByteDance announced the release of 小云雀 ‘little sparrow, an AI-native drama platform. It accepts scripts up to 100,000 characters and is described as the first industry agent powered by Seedance 2.0. Industry leaders have reflected on how Seedance 2.0 has truly solved three previously perceived pain points for AI short-form drama: character/scene consistency, realism in complex physical motion, and continuity/rationality of camera movement.

In an interview with Chinese tech media Jiemian, Chinese filmmaker Gong Changhu told Jiemian that before Seedance 2.0 his 10-person team could produce a 120-minute short drama in 20 days; after Seedance 2.0, that time dropped to half, showcasing how the launch of such AI models could materially raise production efficiency and could trigger explosive industry growth.

A recent Kuiashou Kling press release stated that, since its launch in June 2024, their video generation models have served 60 million creators worldwide and produced over 600 million pieces of content. The press release frames Kling 3.0 as a shift from a “generation tool” to an “intelligent creative partner” that can grasp artistic intent and turn ideas into reality, effectively positioning it as an era in which anyone can turn ideas into films. AI is being sold less as a tool and more as something that takes intent and executes, a true partner in production.

What will AI-empowered micro dramas look like?

Microdrama exporters continue to rapidly capture traffic, scale, and distribution, both in China and abroad. The “second half” of the battle is the efficiency of AI adoption and the ecosystem flywheel effect. For companies like ReelShort, with a huge existing MAU base, the thinking is that once they can cut production costs, they can push out cheaply made content through existing distribution and monetize.

The likely new business model for AI-empowered micro-dramas will be built on a legacy supply chain. It’s about content ownership, character and language localization, lowering expectations, and using AI to cut costs and increase efficiency across the whole stack.

Let’s break down the layers of the ecosystem:

Layer 1: scale of writers. The massive popularity of web novels in China since the early 2000s has created a generation of writers trained to maximize retention at all costs: cliffhangers, rapid reversals, and emotional triggers engineered to drive binge behavior. Web novels, like micro dramas, typically lure readers in with a few free chapters before paywalling subsequent releases. Also, like micro dramas, the market is brutally competitive, with hundreds of thousands of active novels competing for readers at any given time. And the universally loved but loathed themes are all the same: Fifty Shades of Grey style CEO-turned-boyfriend, rags to riches, and Cinderella tales.

The Chinese digital literature ecosystem is a large commercial market; the latest official reports estimated that the number of online literature readers was ~575 million as of 2024 and that industry revenues were tens of billions of RMB. This digital literature space encompasses hundreds of thousands of writers. And that huge group of online novel writers has been pivoting to write micro-drama screenplays in swarms since 2023 as the vertical offers more monetary reward.

Layer 2: IP owners and product creators. The second layer of the supply chain comprises IP owners and product creators. Companies like ReelShort aren’t just microdrama producers. They are part of a larger ecosystem. The studio behind Reelshort is Crazy Maple Studio, which is 49% owned by COL Group (中文在线), a Chinese content company with an enormous inventory of stories ready to be adapted. And they work with writers in both forms: employees for the companies, as well as licensing/buying out webnovel IPs.

For context, COL was founded in 2000 and is listed on the Shenzhen Stock Exchange (stock code 300364). It is said to have more than 5.6 million pieces of digital content and more than 4.5 million digital-native authors. Its products include online books, movies, audiobooks, music, and more. The sheer scale of its IP ownership is an advantage of its own.

Layer 3: tools. The third layer comprises the tools. Chinese short-video platforms have positioned themselves to capture this market, leveraging their in-house data, such as ByteDance’s Seedance model and Kuaishou’s Kling. While both platforms have massive monthly user bases, the vast amount of video and image data they have for training has given them an advantage. Thus, their open-source/open-weight text-to-image models have become competitive with Western industry leaders, such as Veo, Sora, and Midjourney. Not only that, but tools such as Kling and Seedance are largely free for short-form video creation.

Kuaishou’s Kling is targeting independent filmmakers and indie studios to empower them with AI. They’ve also been partnering up with film festivals across Asia, from Hong Kong to Tokyo. ByteDance’s video generator is currently widely available across its AI apps, such as Douban, Jimeng, and Jianying/CapCut, and all at no cost.

Layer 4: distribution. And the final layer is the distribution. Although companies like Reelshort are still largely loss-making, their goal is to blitzscale distribution and then move to profitability. On the first goal, they are doing tremendously well: Reelshort is one of the top apps in the App Store entertainment category, directly competing with top-tier streaming apps for downloads. The logic of Reelshorts is to own distribution, reduce production costs through AI video generation apps, and then reach profitability.

Quibi demonstrated that cramming prestige TV Hollywood economics into short-form doesn’t work — but ReelShort’s bet is the inverse: own distribution, drive production costs toward zero with AI, and let one breakout hit cover the rest.

An article in the Hong Kong newspaper Ta Kung Pao offered a case study that reads like a DTC marketer’s dream: a micro-drama titled The Divorced Billionaire Heiress, reportedly costing under $200k and generating $35 million at the North American box office — 170× returns. Even if you treat that as an extreme example rather than the median, it explains why capital keeps wandering into this “unsexy” corner of entertainment. With AI video generation lowering per-unit production costs, Chinese microdrama platforms have the potential to be able to leap abroad into Western markets.

AI Micro-dramas, a New Soft Power

Television reshaped the movie industry: stories had to move from big screens to the little boxes in our homes, and with this new medium came the rise of the TV series, which challenged the two-hour movie formula. The internet and the rise of streaming changed how we consume those series. Now, micro-dramas are a new business model, natively built for the mobile era. While still niche, they represent a growing source of competition with mainstream streaming services for eyeballs.

While Western studios are still worried about AI taking actors’ or writers’ jobs, Chinese studios are building new micro-drama platforms that are uniquely positioned to leverage AI tools to more effectively capture user attention in the global attention economy. AI-powered microdramas represent a uniquely Chinese vertical, from AI models to distribution platforms, and potentially present a new form of soft power export, following the footsteps of Labubus.

| A guest post by

|